Why the Middle East Gaming Market is Outpacing Global Growth in 2026

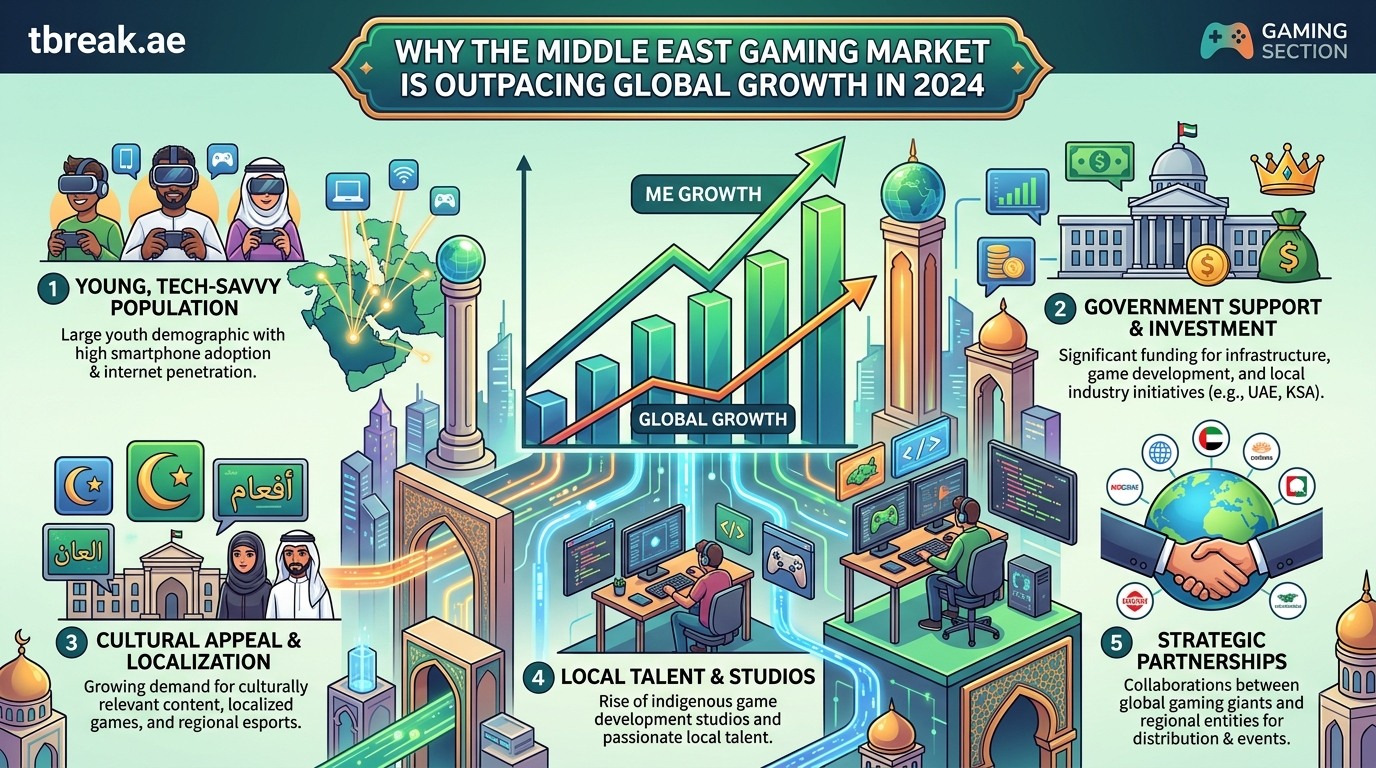

The Middle East gaming market is growing at a pace that makes global averages look sluggish. While worldwide gaming revenue inches forward at single-digit rates, the MENA region is posting double-digit growth year after year. This isn’t a temporary spike. It’s a structural shift driven by demographics, infrastructure investment, and cultural change.

Middle East gaming market growth is outpacing global benchmarks, driven by a young population, massive infrastructure spending, and government-backed esports initiatives. The region’s mobile-first approach, rising disposable income, and cultural acceptance of gaming as entertainment create unique opportunities for developers, publishers, and investors seeking high-growth markets with untapped potential and strong monetization rates.

The numbers tell a compelling story

The MENA gaming market generated over $2 billion in revenue during 2024, with Saudi Arabia, UAE, and Egypt leading the charge. That figure represents a 15% year-over-year increase, nearly triple the global growth rate of 5.6%.

Saudi Arabia alone accounts for roughly $960 million of that total. The kingdom’s Vision 2030 initiative has positioned gaming and esports as strategic priorities, with billions allocated to tournament infrastructure, team sponsorships, and game development studios.

The UAE follows closely with approximately $653 million in gaming revenue. Dubai and Abu Dhabi have become regional hubs for gaming events, attracting publishers and developers who see the Emirates as a gateway to the broader Middle Eastern market.

Egypt rounds out the top three with around $387 million, driven primarily by mobile gaming. The country’s large, young population and improving internet infrastructure make it a high-volume market despite lower average revenue per user compared to Gulf states.

Demographics create a perfect storm

The Middle East has one of the youngest populations globally. Nearly 60% of residents are under 30 years old. This demographic reality translates directly into gaming engagement.

Young consumers grew up with smartphones and broadband internet. Gaming isn’t a novelty for them. It’s a primary form of entertainment, socialization, and even career aspiration.

The region now hosts 168 million gamers, making it the second-largest player base worldwide after Asia-Pacific. That number is projected to reach 200 million by 2026, creating a massive addressable market for publishers.

Average session times in MENA exceed global benchmarks by 23%. Players in Saudi Arabia and UAE spend an average of 11.4 hours per week gaming, compared to 8.7 hours globally. This increased engagement drives higher monetization opportunities through in-app purchases, subscriptions, and advertising.

Mobile dominates the landscape

Mobile gaming accounts for 78% of all gaming revenue in the Middle East. Console and PC gaming have their audiences, but smartphones are the primary platform for the vast majority of players.

This mobile-first reality shapes everything from game design to payment infrastructure. Successful titles in the region prioritize touch controls, shorter session formats, and social features that work well on handheld devices.

Popular genres include battle royale shooters, strategy games, and sports titles. PUBG Mobile, Free Fire, and FIFA Mobile consistently rank among the top-grossing apps across MENA app stores.

Payment preferences lean heavily toward digital wallets and carrier billing. Credit card penetration remains relatively low in some markets, making alternative payment methods essential for maximizing conversion rates.

For hardware enthusiasts looking to upgrade their setup, options like [best gaming laptops under 5000 AED available in UAE and Saudi https://tbreak.ae/best-gaming-laptops-under-5000-aed-available-in-uae-and-saudi-arabia/) provide accessible entry points for serious gamers.

Government backing changes everything

Saudi Arabia’s Public Investment Fund has committed over $38 billion to gaming and esports initiatives. That’s not a typo. Billions with a B.

The Savvy Games Group, a PIF subsidiary, is acquiring game studios, funding esports tournaments, and building physical gaming infrastructure. The Gamers8 festival in Riyadh featured a $45 million prize pool in 2024, making it one of the largest esports events globally.

The UAE has taken a different but equally aggressive approach. Free zones like Dubai’s twofour54 and Abu Dhabi’s Hub71 offer tax incentives, streamlined licensing, and access to regional distribution networks for gaming companies.

Egypt’s government has launched initiatives to support local game development through grants, training programs, and partnerships with international publishers. The goal is to transform Egypt from a consumer market into a production hub.

Investment capital is flooding in

Venture capital firms and strategic investors are pouring money into MENA gaming startups. Funding rounds that would have seemed impossible five years ago are now routine.

Regional publishers like Tamatem Games have raised significant capital to localize international titles for Arabic-speaking audiences. The company has published over 50 games with more than 150 million downloads.

Esports organizations are attracting sponsorships from non-endemic brands. Telecom providers, banks, and consumer goods companies see gaming as a way to reach young, affluent consumers who ignore traditional advertising.

The investment thesis is straightforward: high growth rates, young demographics, rising disposable income, and government support create conditions for outsized returns.

Cultural shifts accelerate adoption

Gaming was once viewed skeptically in many Middle Eastern households. Parents worried about screen time, academic performance, and social isolation.

That perception is changing rapidly. Professional gamers are becoming celebrities. Esports tournaments fill stadiums. Universities are offering scholarships for competitive gaming.

The Saudi Esports Federation now operates national teams that compete internationally. Players who excel in games like Dota 2 and League of Legends represent their countries the same way athletes do in traditional sports.

This cultural acceptance removes barriers to market growth. Parents who once restricted gaming time now see it as a legitimate hobby or even career path.

Localization matters more than you think

Arabic language support isn’t optional in this market. It’s essential. Games that offer proper Arabic localization see conversion rates 3x higher than English-only titles.

But localization goes beyond translation. Successful publishers adapt content to respect cultural norms, adjust monetization strategies to match regional preferences, and engage with local influencers who understand the audience.

Character designs, storylines, and even color schemes may need modification. What works in Western markets doesn’t always translate directly.

Regional events and seasonal content tied to Ramadan, Eid, and other cultural moments drive significant engagement spikes. Publishers who plan content calendars around these dates see measurable revenue increases.

Practical steps for market entry

Companies looking to capitalize on Middle East gaming market growth should follow a structured approach:

-

Start with market research specific to the target country. Saudi Arabia, UAE, and Egypt have different player preferences, payment behaviors, and regulatory environments.

-

Partner with regional publishers or distributors who understand local nuances. Going it alone rarely works for first-time entrants.

-

Invest in proper Arabic localization, including right-to-left text support, culturally appropriate content, and local customer support.

-

Implement payment methods that match regional preferences, including carrier billing, digital wallets, and local payment cards.

-

Build relationships with influencers and content creators who have established audiences in your target markets.

Key differences across MENA markets

| Market | Primary Strength | Average ARPU | Preferred Genres | Payment Method |

|---|---|---|---|---|

| Saudi Arabia | Highest spending power | $87/year | Battle royale, sports | Credit cards, Apple Pay |

| UAE | Most diverse player base | $72/year | Strategy, racing | Digital wallets, cards |

| Egypt | Largest player volume | $18/year | Casual, mobile RPG | Carrier billing, prepaid |

| Qatar | Highest engagement rates | $94/year | Sports, shooters | Credit cards |

| Kuwait | Strong esports culture | $81/year | Competitive multiplayer | Digital wallets |

Common mistakes to avoid

New entrants frequently stumble in predictable ways:

- Treating MENA as a single homogeneous market rather than recognizing country-specific differences

- Launching with English-only interfaces and expecting strong adoption

- Ignoring payment method preferences and losing conversions at checkout

- Failing to account for Ramadan’s impact on playing patterns and spending

- Underestimating the importance of local influencer partnerships

- Copying Western monetization strategies without testing regional variations

What industry professionals are saying

“The Middle East represents the last major untapped gaming market with both scale and spending power. Companies that establish strong positions now will benefit for decades as the market matures and expands.” — Regional gaming analyst with 15 years of MENA market experience

This perspective reflects broader industry sentiment. The window for early-mover advantage is still open, but it’s closing as more publishers recognize the opportunity.

Infrastructure improvements accelerate growth

Internet penetration across the Gulf states now exceeds 98%. Average connection speeds have improved dramatically, with 5G networks rolling out across major cities.

Saudi Arabia’s NEOM project includes plans for dedicated gaming and esports facilities. The UAE is building purpose-designed arenas for competitive gaming events.

Cloud gaming services are gaining traction as infrastructure improves. Latency issues that once made streaming games impractical are becoming manageable in major urban centers.

These infrastructure investments create conditions for more sophisticated gaming experiences. Mobile will remain dominant, but console and PC gaming have room to grow as connectivity improves.

The esports ecosystem is maturing fast

Professional esports organizations now operate across multiple MENA countries. Teams compete in regional leagues with prize pools that rival traditional sports.

Sponsorship revenue for esports events in the region grew 156% between 2022 and 2024. Non-endemic brands see esports as a way to reach young consumers who avoid traditional media.

Universities in Saudi Arabia and UAE now offer esports programs and scholarships. This institutional support legitimizes competitive gaming and creates career pathways for talented players.

Viewership numbers for major tournaments routinely exceed 10 million concurrent viewers across streaming platforms. That’s an audience size that commands serious advertising dollars.

Monetization strategies that work

Successful games in the MENA market typically employ these tactics:

- Battle passes with regional pricing that accounts for purchasing power differences

- Limited-time offers tied to cultural events and holidays

- Social features that encourage group play and gift-giving between friends

- Cosmetic items that allow self-expression without creating pay-to-win dynamics

- Subscription models with family sharing options

- Localized payment options that reduce friction at checkout

Average revenue per paying user in Gulf markets exceeds global benchmarks by 34%. Players who do spend tend to spend more, making user acquisition costs easier to justify.

Regulatory landscape remains favorable

Most MENA countries have gaming-friendly regulatory environments. Content restrictions exist, but they’re generally predictable and manageable.

Age ratings follow international standards with some additional content guidelines. Violence, gambling mechanics, and certain themes may require modification.

Data privacy regulations are evolving but remain less stringent than GDPR. Publishers should still implement strong data protection practices to build trust.

Tax structures vary by country, with free zones offering significant advantages. Professional legal and tax advice is essential for optimizing market entry strategy.

What the next three years look like

Projections show the Middle East gaming market reaching $3.2 billion by 2027. That represents a compound annual growth rate of 15.8%, maintaining the region’s position as the world’s fastest-growing gaming market.

Saudi Arabia will likely surpass $1.5 billion in annual gaming revenue as Vision 2030 initiatives mature. The country’s ambition to become a global gaming hub is backed by resources that few regions can match.

Mobile will remain dominant but console and PC gaming should gain market share as infrastructure improves and more households purchase dedicated gaming hardware.

Esports will continue professionalizing, with regional leagues, permanent venues, and career development programs creating a sustainable ecosystem.

Why this matters for your business

The Middle East gaming market growth story isn’t about potential anymore. It’s about execution.

The fundamentals are in place: young demographics, rising incomes, government support, improving infrastructure, and cultural acceptance. Companies that enter this market with proper localization, regional partnerships, and patient capital will capture outsized returns.

The window for early-mover advantage is still open, but major publishers are already establishing positions. Regional players are getting sophisticated. The competitive landscape is evolving rapidly.

For gaming industry professionals, investors, and business development managers, the question isn’t whether to enter the MENA market. It’s how quickly you can execute a credible market entry strategy before the opportunity becomes crowded.

The data is clear. The momentum is undeniable. The Middle East gaming market is outpacing global growth, and that trajectory shows no signs of slowing.

Post Comment